One of the safest investments in Nepal is doing a Fixed Deposit (FD) in Banks. It’s one of the classical ways of getting the best risk-free returns in Nepal, practiced by most of the old-age citizens (but not limited to). So, if you are planning to lock your savings away for guaranteed then here you can go with this FD Calculator before you commit your money to the bank. By using our calculator, you will know exactly what you’ll get back at the end of your term. Our FD Calculator makes it incredibly easy to project your interest earnings and total maturity amount. Whether you are comparing rates across different commercial banks or deciding on the best timeframe for your goals, this Fixed Deposit Calculator gives you instant, accurate numbers to help you make a confident financial decision.

FD Calculator Nepal

Fixed Deposit with NRB quarterly compounding · TDS · Premature withdrawal · Payout options

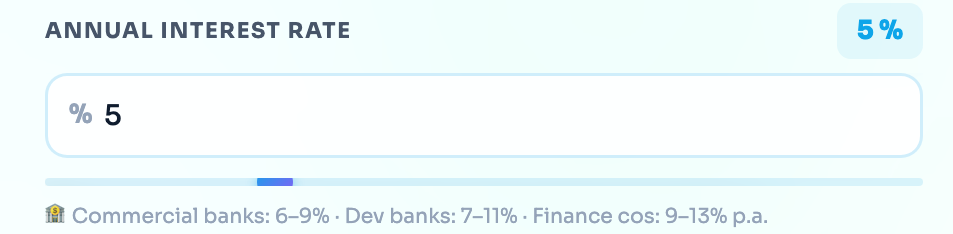

🏦 Commercial banks: 6–9% · Dev banks: 7–11% · Finance cos: 9–13% p.a.

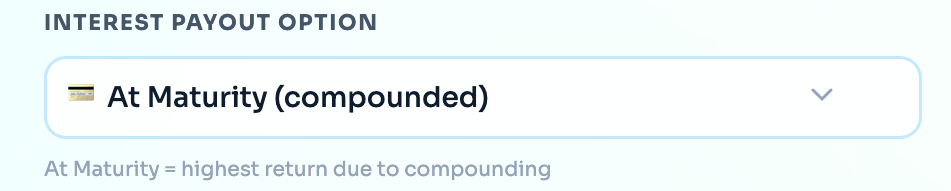

At Maturity = highest return due to compounding

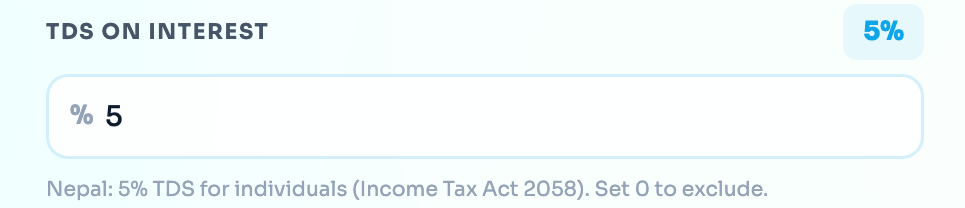

Nepal: 5% TDS for individuals (Income Tax Act 2058). Set 0 to exclude.

Nepal banks deduct 1–2% from rate if broken before maturity

💳 Periodic Payout Amount

| Period | Opening (रू) | Interest (रू) | TDS (रू) | Closing (रू) |

|---|---|---|---|---|

| Click Calculate to see breakdown | ||||

📖 Nepal FD Rules (NRB Guidelines)

- Compounding: Nepal Rastra Bank (NRB) mandates quarterly compounding for all bank fixed deposits.

- Minimum tenure: 1 month. Most Nepal banks offer FD from 1 month to 10 years.

- Interest rates (2024–25): Commercial banks: 6–9% · Development banks: 7–11% · Finance companies: 9–13% p.a.

- TDS: 5% Tax Deducted at Source on all interest income for individuals under Nepal Income Tax Act 2058, Section 87. Institutions may have different rates.

- Premature withdrawal: Banks deduct 1–2% from the applicable interest rate if FD is broken before maturity. Your principal is 100% safe.

- Interest payout: Nepal banks offer At Maturity (highest yield due to compounding), Monthly, Quarterly, Half-Yearly, or Annual payout options.

- Auto-renewal: Most Nepal banks auto-renew FD at prevailing rate on maturity. Issue a written request to close on maturity.

- Deposit insurance: Nepal Deposit and Credit Guarantee Corporation (DCGC) insures deposits up to रू 5 lakh per depositor per bank.

⚠️ Rates shown are indicative. Actual rates vary by bank, tenure, and amount. Verify with your bank before investing. Not financial advice.

How to use the FD Calculator

A Fixed Deposit (FD) is a staple for secure investing in Nepal. Locking your principal amount in a lump sum for a specific period with a fixed interest rate to get a guaranteed return is one of the best ways of saving. Our FD Interest Calculator helps you to calculate the actual return that you to how to use it to plan your investments easily.

Step 1: Enter Your Principal Amount

- Principal Amount (NPR): This is your initial investment. Type in the total lump sum amount that you plan to deposit into the FD account. Here, for reference, we set it as 10,00,000 (10 Lakh or 1 Million)

Step 2: Set Your Interest Rate

- Annual Interest Rate: Enter the exact interest rate your bank is offering. If you are searching around, keep in mind that rates generally differ by the type of institution:Commercial Banks: Generally offer lower than Dev. Banks and Finance Companies.

- Development Banks: Often give a bit more than or equals to Commercial Banks.

- Finance Companies: Usually offer the highest rates compared to both A & B Class Banks.

Step 3: Choose Your Tenure

- FD Tenure: How long do you want to lock your money away? Enter the number of months. Banks in Nepal offer flexible tenures, anywhere from 3 months up to several years. In our system, it only has the option of Months (not years), so if you are planning to do this FD for more than years, then use that time period by converting it into months, like for 2 years of FD, we have to enter 24 Months (which is the same and equivalent to the given years or months).

Step 4: Select Your Payout Preference

- Interest Payout Option: Use the dropdown to choose how you want to receive your earnings interest. Generally, the Nepali Banks share the interest on your FD every 3 closing months (End of Ashad, Ashwin, Poush & Chaitra or at the maturity date). Also, Leaving at Maturity (compounded) means your interest earns interest, giving you the absolute highest return when the FD ends. So, you can choose Quarterly Payout.

- If you rely on your FD for regular income, you might select a monthly or quarterly payout instead (though your final maturity amount will be lower since the interest isn’t compounding).

Step 5: Factor in the Taxes

- TDS on Interest: The Government of Nepal mandates a 5% Tax Deducted at Source (TDS) on interest earned by individuals (Income Tax Act 2058). We’ve set the default to 5% so you see your actual, take-home money. If you are calculating for an institution with a different tax bracket, or just want to see the gross amount, you can set this to 0 so the FD Calculator gives the accurate result.

Step 6: Consider the Premature Penalty (Optional)

- Premature Withdrawal Penalty: Every bank offers a premature withdrawal feature. So, if you need your money before the tenure ends, then you can do it manually from the Mobile Banking Apps. Most of the Nepali banks typically deduct a 1% to 2% penalty from your applicable interest rate for breaking the lock-in period. Adjusting this field lets you see exactly how much an early withdrawal would cost you. Remember: It’s different from Loan Against FD (LAFD)

Step 7: See Your Total Growth. Just click the Calculate FD Returns button. You will instantly see your final maturity amount and total interest earned, so you know exactly how hard your money is working for you.

“These are estimates only. Consult a SEBON-registered advisor before investing.”