SIP Calculator is a free online tool designed to help every Nepali investor guide them with an easy calculator to calculate their returns based on their investment value and planning. Using this SIP Calculator Nepal, you can easily use all features online to calculate your plan before investing in any mutual fund schemes offered by Issue Manager.

Free SIP Calculator Nepal

SIP · Lumpsum · Step-Up SIP — Accurate Nepal investment formulas

💡 Nepal equity mutual funds historically return 10–18% p.a.

| Period | Invested (रू) | Returns (रू) | Total Value (रू) | Gain % |

|---|---|---|---|---|

| Calculating… | ||||

SIP is a systematic way of investing your money in mutual funds. SIPs are open-ended mutual funds. It’s a way of investing money in targeted capital or Investment company mutual fund schemes offered by the Issue Manager and Capital Companies. In simple terms, SIP is a systematic plan to invest at a preset frequency for an ongoing process, without considering market conditions or knowing the complete details of Mutual funds and investments. That’s why SIP is called a Systematic Investment Plan.

Complete Guide to SIP Investing in Nepal

If you are the investors and want to calculate the returns as of. now or the new one planning to start investing in mutual fund as SIP then this calculator will be the best online tool for you. With this free calculator you can easily calculate the returns with different methods as by with expected rate of return, monthly investment amount and desired tenure (no. of years) as per your requirement.

What Is SIP (Systematic Investment Plan)?

SIP (Systematic Investment Plan) is a preset habit of investing a fixed amount of money regularly (monthly, quarterly, semi-annually, or annually) in mutual funds. In practice, it’s the process of buying the specific units of mutual funds (schemes) from an issue manager like Nabil Investment for NI31 & Nabil Flexi Cap, or Laxmi Capital for Subha Laxmi Kosh, with your monthly contribution.

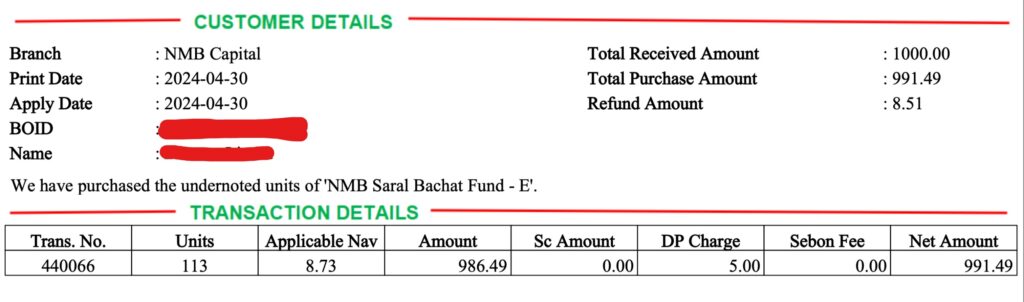

In simple terms, although you invest Rs 1000 monthly, for example, in NI31 by Nabil Investment, you pay Rs 1000 to Nabil Investment every month for your NI31 Scheme. After paying Rs 1000 to them, you are done on your end, and many of us think I invested Rs 1000 for this month too. But the real practice of mutual funds is not directly investing the rupees (money). Still, a mutual fund is a capital market, so based on the current market value of that mutual fund (may be Rs 11.0 per Unit called NAV in investment terms), in that case, the issue manager separates or purchases the x units up to your monthly investment of Rs 1000, which is around 90 Units only. From your Rs 1000, the issue manager deducts the DP Charge and other fees. As I said earlier, SIPs are open-ended mutual funds, so, as with closed-end (regular mutual fund) funds, the issue manager buys units at the current NAV for you. You can see the image below for this.

SIP Vs One-time (Lumpsum) – Which is Best?

So, now you are clear about SIP Investment. Now let’s talk about the two methods used in investing: SIP vs. lump sum. The choice between a Systematic Investment Plan and a lumpsum investment depends entirely on your cash flow and current cash holdings. Also, depends largely on the market volatility you can stomach.

SIP vs Lumpsum — Quick Comparison

Hope you got it! So which one should you choose?

Go with SIP if:

- You want investment discipline: If you want to set investment discipline, you can go with SIPs, as they make a habit of regular savings or investments.

- You have a regular lump sum: If you are a salaried person or have regular income from any source, then it’s the best investment habit ever for you.

- You are building a corpus: If you plan to achieve long-term goals with minimal regular income, then it’s for you.

- You don’t have a larger investment amount: A one-time investment with a huge amount always wins, but if you don’t have that huge investment amount, then this regular SIP is the way to be smart and wealthier in the future.

Go with a lump sum if:

- You have a windfall: If you receive a good amount from your investment, business, or maybe from closing or a festive bonus, then it will be the best Investment opportunity.

- You have a large investment amount. If you already have a good portion of the amount to invest, go with a lumpsum investment, as it compounds faster each year.

Why SIP Works Well for Nepali Salaried Investors

For salaried investors, freelancers, or regular income holders, the SIP works well and becomes the biggest driver, pulling their small, regular investments into huge savings for the future. As SIPs in Nepal can start with as low as Rs 1000 per month (Rs 500 per month with NIC ASIA Linked Equity Fund), it is a lump sum for very small investors like you, who are currently holding jobs or working independently.

As the SIP is fully pre-customizable as per the investor’s needs, it fits every salary cycle or income credit cycle. That’s why SIP is fully flexible for every job holder and for anyone planning to spend their summer. Also, SIP follows the long-term compounding process; every dividend received is reinvested as principal units to drive higher returns on investment.

Similarly, the SIPs are fully managed by the SEBON-regulated capital market’s experts and their associated companies, such as Nabil Investment Banking and NIC ASIA Capital, so there will be only market risk, excluding other risks.

Note: Returns on mutual funds are not guaranteed. So, please read our Financial Disclaimer.

How SIP Works in Nepal (Step by Step): Requirements for SIP Registration Process

Starting a SIP requires certain steps and requirements that every investor must meet. Here are the steps required.

Open a Demat Account: You only need one. The first requirement for processing SIP is your Demat Account.

Get Mero Share & CRN No. (C-ASBA): After having a Demat Account, you need to register/create a MeroShare Account too, along with C-ASBA Registration. Most banks offer MeroShare registration through their subsidiary companies, such as investment and Capital companies. For C-ASBA, the Bank will register it for you and link it to your DEMAT Account.

Choose SIP Plan: Decide which Open-ended scheme is best for you from the 8 schemes in Nepal offered by different Issue Managers, such as Subha Laxmi Kosh SIP by Laxmi Sunrise Capital, NI21 & Nabil Flexi Cap Fund SIP by Nabil Investment Banking, Siddhartha SIP by Siddhartha Capital, or any other.

Register SIP with Fund Manager: After choosing the SIP Plan/Scheme, visit the Issue Manager SIP Registration page and create a user there, then fill out all the details with your investment requirements. If you want SIP at NIBL Sahabhagia Fund, visit the NIMB Ace Capital SIP Registration Page.

Start Investing: After setting all SIP Plan details, start paying your Monthly SIP using available Payment Methods in checkout. That’s all.

You can click/tap here to learn how to open a SIP Account and here to learn how to pay SIP online easily.

How to use SIP Calculator: Steps for Calculation

So, let’s get into the practical steps to calculate the SIP using our SIP Calculator. Here I have shared the actual steps based on the SIP Calculator on this site.

Step 1: Ensure the Function/tab is set to SIP. By default, it’s chosen as SIP. If not, tap SIP.

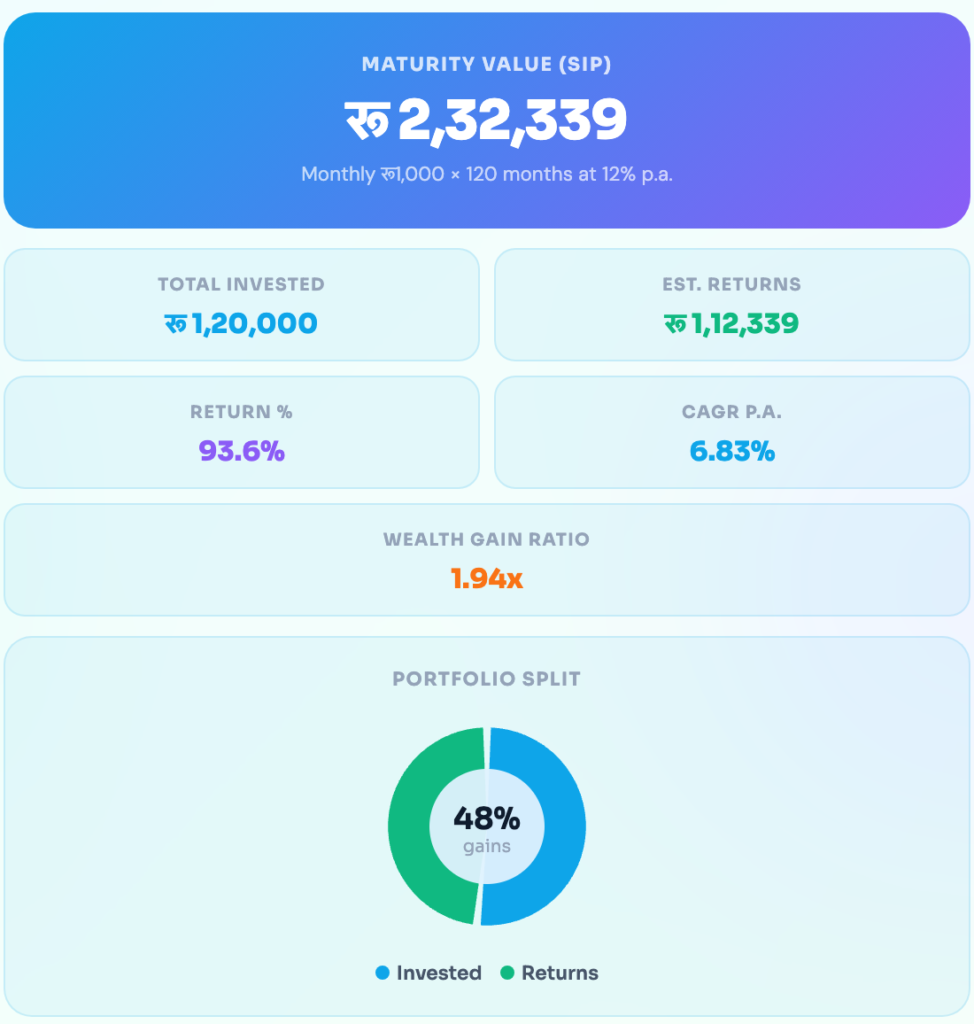

Step 2: Now enter your monthly investment amount. As per your requirement, you can select a scale or enter manually. Here I am selecting Rs 1000.

Step 3: Set the investment Period. Here, for example, I am setting 10 Years. But as per your requirement, you can set any duration.

Step 4: Set the expected return from your mutual fund investment with your issue manager as the dividend.

Step 5: That’s all. Happy Investing! Here you will see the complete details view, with yearly and monthly breakdowns.

Frequently Asked Questions

What is SIP, and how does it work in Nepal?

SIP is a simple investment plan in an open-ended mutual fund with a long-term goal. SIPs work like mutual funds, compounding your investment.

What is the minimum SIP amount in Nepal?

In Nepal, the minimum SIP Amount is Rs 1000 per month. You can start investing in SIPs with as little as Rs 1000 per month. Also, NIC ASIA Balanced Linked Fund offers SIP with a monthly contribution of Rs 500.

How accurate is this SIP calculator?

The SIP Calculator is designed to follow Nepal mutual fund calculation logic and Nepali market calculation logic. So, it’s accurate in calculations, but the return on your investment depends on market conditions, your Issue Manager, and the fund’s status.

Can I change my SIP amount midway?

Yes, most Issue Managers allow investors to customize their existing SIP Plan on their websites easily. So, the investors can do it easily from the user dashboard.

What return rate should I use for mutual funds in Nepal?

There are no fixed returns on SIP mutual funds in Nepal. But according to the last report, they have been giving an average of 10–12% returns so far.

Is this calculator completely free?

Yes, this SIP Calculator NP is completely free to use for everyone. So, start calculating and start investing.

What is NAV, and why does it matter for SIP?

NAV is the Net Asset Value of that Mutual Fund. Based on NAV, your Issue Manager will purchase mutual fund units on your behalf.

How do I redeem my SIP investments in Nepal?

Some issue managers, like Nabil Investment Banking, allow you to redeem the SIP easily from their dashboard. For other users, they must fill out the form and send it to the concerned department of the Issue Manager via mail, or they can also visit their parent company (Bank) to submit the redemption or cancellation form.

SIP investing in Nepal is not about timing the market — it is about staying consistent with your preset investment plan. Use the SIP calculator NP above to plan your SIP for the future goal, read our guides to understand the process, and start with an amount you can sustain every month. That’s all for the SIP Calculator. Thank you!

Mutual fund investments are subject to market risk; treat every projection as an estimate, not a promise.